On May 11, 2021, the US Treasury Department imposed new sanctions on seven individuals associated with Hezbollah and the Al-Qard Al-Hassan Foundation. Previous sanctions were imposed in April 2016.

Al-Qard Al-Hassan (AQAH) literally means “the benevolent loan.” Affiliated with Hezbollah, it is officially a charity and the country’s biggest micro credit organization. However, AQAH has all the functioning characteristics of a bank.

“While AQAH purports to serve the Lebanese people, in practice it illicitly moves funds through shell accounts and facilitators, exposing Lebanese financial institutions to possible sanctions,” the US Treasury Department said in a statement.

“AQAH masquerades as a non-governmental organization (NGO) under the cover of a Ministry of Interior-granted NGO license, providing services characteristic of a bank in support of Hezbollah, while evading proper licensing and regulatory supervision.” Despite US sanctions, Lebanon’s dire economic crisis and the collapse of both the banking system and the Lebanese pound (LBP), AQAH introduced a series of new services in October 2020 and installed ATMs in three of its branches in Beirut’s southern suburbs.

It intends to install more in branches elsewhere.

AQAH also started buying and selling gold against the dollar and providing storage for gold against a low fee to help confront the rising crime rate in areas under the Hezbollah’s influence: Beirut’s southern suburbs, the south of Lebanon and the Bekaa Valley AQAH has started dealing with clients on the basis of the black market dollar exchange rate, which now poses a problem for some borrowers, as they’d taken out a loan at the official exchange rate, which used to be 1500 LBP to the dollar, while today’s rate is much higher than that.

“Dealing with the association, seeing the disasters around you, the country was collapsing, and you were afraid of the threat that they would confiscate your gold,” explained Fadwa, a young Lebanese woman in her twenties, who used to have a loan from AQAH. “Psychologically, it was tough, especially after the lira collapsed [in October 2019].” Due to the sanctions imposed by Washington, most people dealing with AQAH prefer to remain anonymous.

Services

AQAH is specialized in providing relatively small loans for a relatively short period of time. A report published by the Bint Jbeil website in 2010 stated that half of the AQAH clients took a loan to meet their daily needs and 27% to pay off a debt, while the rest intended to pay for housing (6%), hospitalization or education (5%), and marriage or home furnishings (3%).

In October 2019, AQAH launched new loans for small agricultural, industrial and handicrafts projects. The loans’ combined value amounted to some 80 million LBP to be repaid over 60 months, according to an interview with the association’s executive director Adel Mansour.

To profit from an interest-free loan to be repaid within a period of 30 months, the borrower must have a guarantee from an AQAH depositor or hand over gold or jewelry. Borrowers also have to pay a small administrative fee of about $3 a month, either in dollars or LBP (black market rate). They must furthermore deposit $12 a month in an interest-free account. About four out of five dollar loans are backed by gold deposits, while the loan amount never exceeds 70% of the mortgage value, according to AQAH executive director Mansour.

AQAH grants four types of loans:

1- Loans against gold collateral (most common)

2- Monthly loans in return for a guarantee for the participants who deposit funds in the association.

3- Loans against the guarantee of wealthy people.

4- The guarantee provided to the borrower for the purpose of purchasing goods and services from institutions

AQAH claims its depositors belong to many different sects. Yet, according to Joseph Daher, assistant professor at the University of Lausanne and author of the book Hezbollah: The Political Economy of The Party of God, that is inaccurate: depositors from outside the Shiite environment are the exception rather than the rule.

What’s more, all AQAH branches are located in predominantly Shiite areas and the organization is frequently deployed in activities and campaigns related to Hezbollah.

Black Market

While Lebanese banks are floundering, the AQAH saw depositors and activities increase significantly. It furthermore entered the “black market game,” as AQAH obliged borrowers to repay their loans according to the black market exchange rate.

“I pawned $1,500 in gold to take out a loan,” said Fadwa. “The process was very easy, with 0% interest. The only condition was that I repay the value of the loan and freeze $200 at the AQAH for one year. This was before the dollar crisis.” After the collapse of the LBP, however, repayment became much more difficult for Fadwa. “Because my pension is in Lebanese pounds, the cost of repayment doubled and continued to rise. So, I decided to do the repayment quickly to avoid even larger amounts.”

“AQAH should have found a way to stabilize the exchange rate, because it does not make sense to take out a loan at 1,500 LBP to the dollar and having to pay it back at the current black market rate,” she added.

In his speech on Martyr’s Day on November 11, 2020, Hezbollah Secretary-General Hassan Nasrallah boasted that anyone withdrawing savings from Lebanese banks and depositing them at AQAH would preserve his or her money. His comparison places AQAH in the category of Lebanese banks.

In his January 2021 speech Nasrallah said that US sanctions against Hezbollah officials had in fact strengthened AQAH, as many of them had decided to transfer their accounts from Lebanese banks to AQAH. Nasrallah defended the association and considered that everyone who deposited his money at AQAH would, firstly, serve the people and, secondly, preserve one’s money, and thirdly, earn wages and rewards as a partner in lending.

“If one day it is in need, we support it,” Nasrallah said. “We support the AQAH. It is not the AQAH that supports us.”

During the onset of the banking crisis, “MBC” transferred her money to two accounts at the AQAH. “A lot better and more comfortable than a normal bank,” she said.

“I don’t want to withdraw from AQAH, but if I do, I want it in dollars,” she said. “As for loans, many people today suffer from the difference in the exchange rates and curse AQAH for it.”

Charges

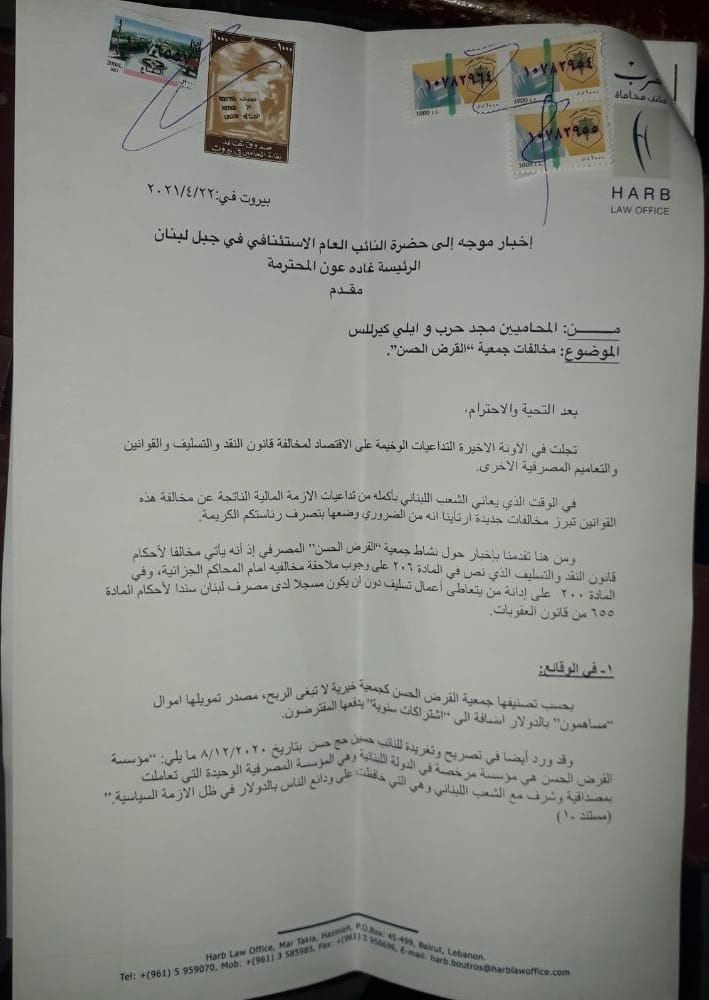

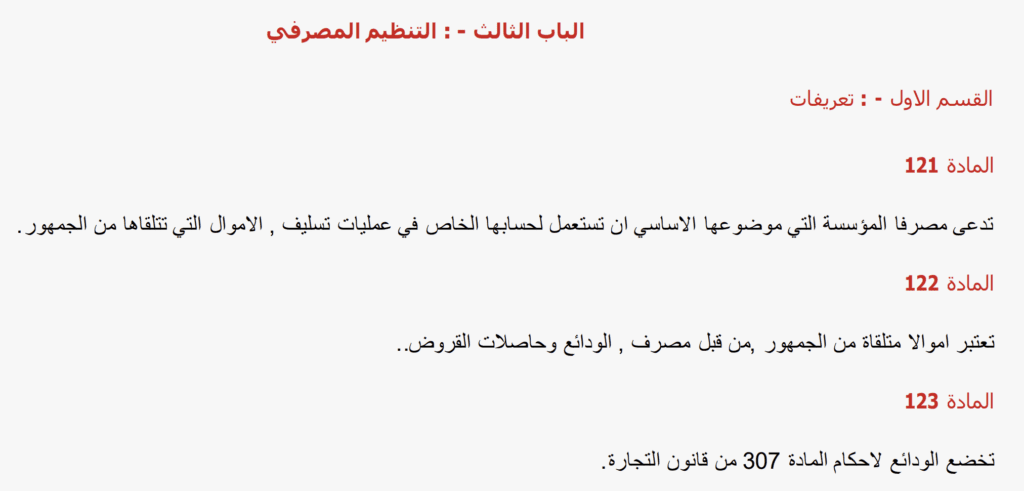

On April 22, 2021, Lebanese lawyers Majd Harb and Elie Kirlos filed a complaint with Mount Lebanon Public Prosecutor Ghada Aoun against AQAH for violating the provisions of the Code of Money and Credit, which stipulates that those engaging in credit activities need to be registered with the Banque du Liban (BDL).

The BDL Basic Circular 93 in article 7 furthermore states that “microcredit institutions are granted a time limit expiring on 31 July 2019 to adjust their situation, particularly to transfer or liquidate the loans they have directly granted before August 16, 2018.”

As for the AQAH’s ATMs, this violates BDL Basic Circular 36, which states in Article 1: “Banks and bank-owned institutions are allowed to set up, install and operate an automated teller machine in the place they deem fit, provided that they notify Banque du Liban in advance …”

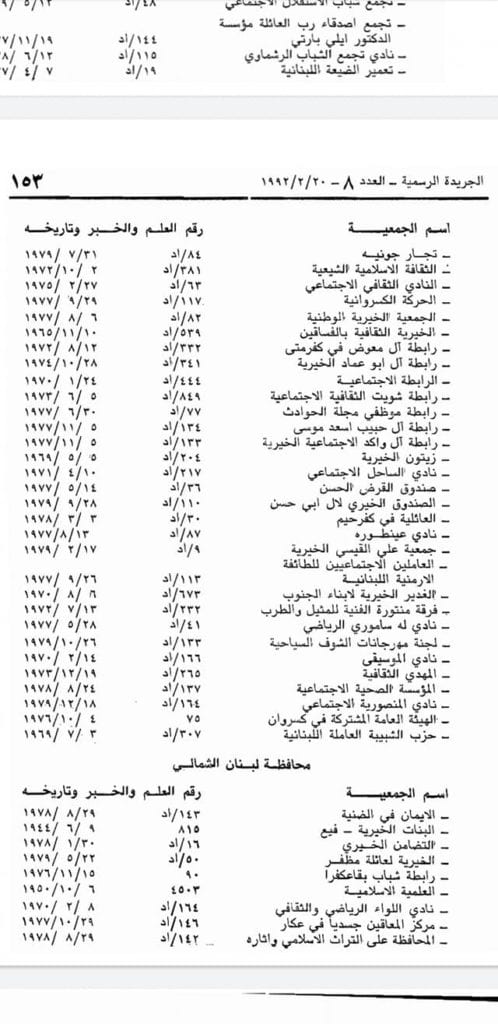

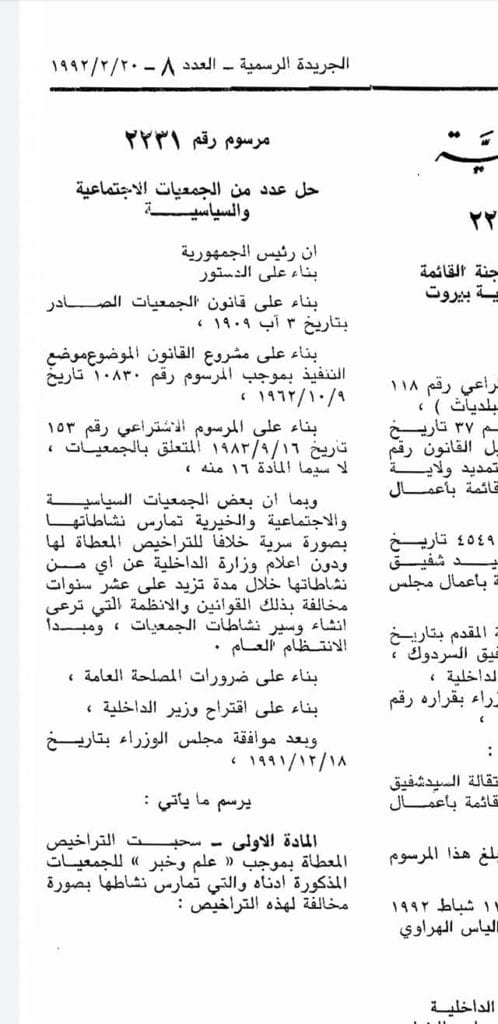

The Lebanese law prohibits practicing the banking profession without a prior license from the BDL. It should be noted that Decree No. 2231 issued in 1991 withdrew the licenses of Al-Ilm wa Al-Khabar for many associations due to their activities in violation of these licenses. AQAH was one of them.

AQAH and the Banks

In December 2020, the anonymous hacker group SpiderZ revealed links between some Lebanese banks and AQAH. They included Jammal Trust Bank, Credit Libanais, Byblos Bank and others.

Joseph Daher noted that Hezbollah, only after the collapse of the Lebanese banking system, started to attack BDL Governor Riad Salameh through Nasrallahs speeches. For years, the party contributed to extending Salameh’s mandate, despite the tension and several verbal altercations following the US imposing sanctions.

According to the Al-Akhbar newspaper, the party at one point in 2016 sent a positive message to Salameh “in appreciation of his role in curbing some banking institutions and preventing them from turning American law into a tool to punish the environment of the resistance.”

According to Daher, this was due to the fact that Salameh, despite applying international sanctions against Hezbollah, preserved the AQAH and, to some extent, protected Hezbollah’s interests. Hezbollah also refused the idea of removing Salameh from his position as BDL governor.

While there is no direct relationship, the BDL condones AQAH’s “illegal banking” activities. We contacted the Banking Control Commission of Lebanon at the BDL several times, yet did not get a response.

According to Daher, the AQAH’s capital has increased since 2019, as the Lebanese, especially the Shiites, deposited their money at the AQAH rather than in regular banks. Adding: “There is a continuation of the building of the state of Hezbollah, which is benefiting from the current crisis.”

“In the light of the current crisis, AQAH has become the only financial institution that, firstly, still provides loans and, secondly, loans in hard currency,” said Mohanad Hage Ali, director of communications and a fellow at the Malcolm H. Kerr Carnegie Middle East Center. “AQAH has become the only banking entity still performing this function, as the banks involved with the public debt are facing illiquidity and have become absent.”

Sources of Funding

AQAH seeks to finance itself through the commissions paid by borrowers ($3 per monthly payment). Other sources of funding are donations and membership fees. Some media have hinted at external sources of financing, specifically Iranian, but there is no evidence to back up such claims.

However, the institution’s ability to deal in hard currency at a time when other commercial banks are unable to do so raises some questions, whereby it is worth noting that the institution operates outside the country’s financial system.

“The association’s growth must be attributed to two factors,” Mohanad Hage Ali speculated. “Firstly, liquidity from abroad, through Iran or Iranian institutions. And secondly, employment in the institution, and its management, are part of the party structure and therefore not included in the budget.”

The Good Loan

Since October 2019, that is, since the beginning of the economic crisis, depositors have withdrawn about $6 billion from Lebanese banks. According to Nasrallah, part of this money was deposited at AQAH, which is evident seeing the increase in deposits in 2019 and 2020.

However, AQAH is still classified as a charitable association, even though there are several Islamic banks in Lebanon, which provide banking services that comply with Islamic law. How does AQAH differ from them?

AQAH describes itself not as a bank, but as “charitable non-profit association.” However, according to the information submitted against the association: “a simple change of terminology does not change the legal nature of the institution, meaning that replacing ‘bank’ with ‘association’ or ‘depositor’ with ‘shareholder’ does not negate the existence of banking activity without the necessary licenses.”

“The institution does not carry out any commercial or investment activities, and it does not have a profitable purpose at all,” said Nasrallah in his speech in January 2021. “And this is the difference between AQAH and normal banks. It is an essential difference.”

Law No. 575, issued on February 11, 2004 regulates the manner of establishing Islamic banks in Lebanon, which states must obtain a license from the BDL Central Council.

The bank that receives a sum of money as a deposit becomes its owner and must return it with an equivalent value in one or several payments at the depositor’s first request or according to the terms regarding time limits and prior notification, as specified in the contract.

It is predominantly the Code of Money and Credit that governs the banking sector, which bans any real or legal person who does not practice the banking profession from receiving deposits.

Volume of Transactions

Nasrallah described the association as “steadfast, stable, strong and solid.” According to him, since its foundation, it has provided some $3.7 billion in loans to 1.8 million people, while currently some 300,000 people have a loan from the association.

In a previous interview, AQAH CEO Adel Mansour said that deposits doubled in 2020, while in 2019 more than 200,000 loans were granted. With an average value of $2,500 per loan, total value amounted to a record $500 million. AQAH has over 30 branches across Lebanon and some 500 employees.

Our reporter tried to communicate with the AQAH media office more than once, but the latter did not respond before the report was published.

Sanctions

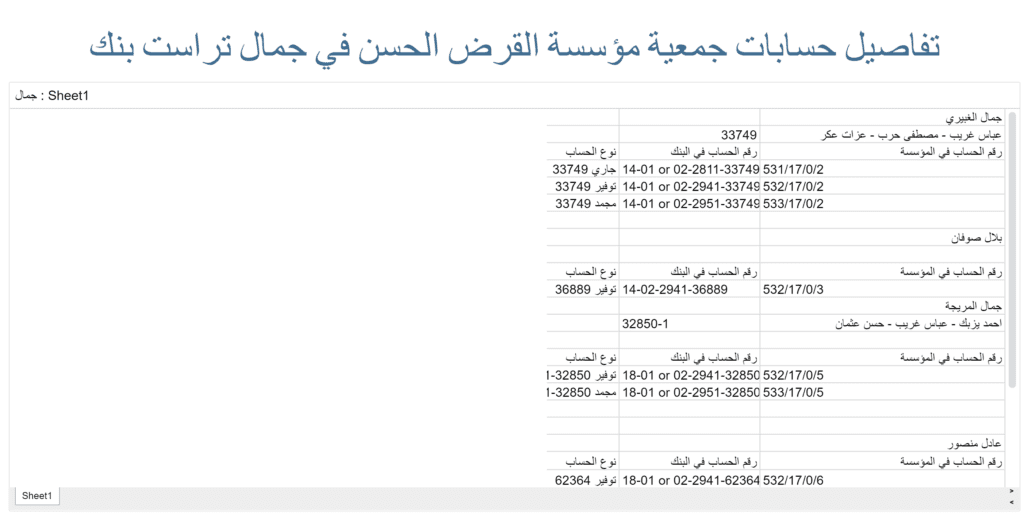

On May 11, 2021, the US Treasury imposed new sanctions on individuals associated with Hezbollah and AQAH, most notably financial director Ahmed Muhammad Yazbek and IT director Abbas Hassan Gharib, in addition to Abbas Hassan, Mustafa Habib Harb, Waheed Mahmoud Sbeity, Hassan Shehadeh Othman and Izzat Yusef Akar “due to their dealings, directly or indirectly, for or on behalf of AQAH.”

The US Treasury had previously targeted Hezbollah’s Martyr’s Institute and AQAH on July 24, 2007, by classifying them as organizations supportive of Hezbollah. In April 2016, the US Treasury included AQAH on the list of Hezbollah institutions subject to sanctions.

Historical background

AQAH relies on Surat Al-Hadid, verse 11 for its loan and banking work, which states: “Whoever lends God a goodly loan, God will increase it manifold (to his credit), and he will have an honorable, generous reward.” AQAH relies on Surat Al-Hadid, verse 11 for its loan and banking work, which states: “Whoever lends God a goodly loan, God will increase it manifold (to his credit), and he will have an honorable, generous reward.”

“The Al-Qard Al-Hassan Association was established in 1982, following the Israeli invasion of Lebanon and the devastating social and economic conditions that followed, to be one of the tributaries of the resistance through its support for the Lebanese resistance community,” thus reads the AQAH website. It received a license as a charitable organization from the Ministry of Interior in 1987.

A State of Concern

Both Daher and Hajj Ali think it likely that Hezbollah is worried about the deterioration of the economic situation within the Shiite community, especially among loyalists. Recently the party issued the “carpet card” for purchases, which works as a credit card, but its scope is limited to certain shops and institutions.

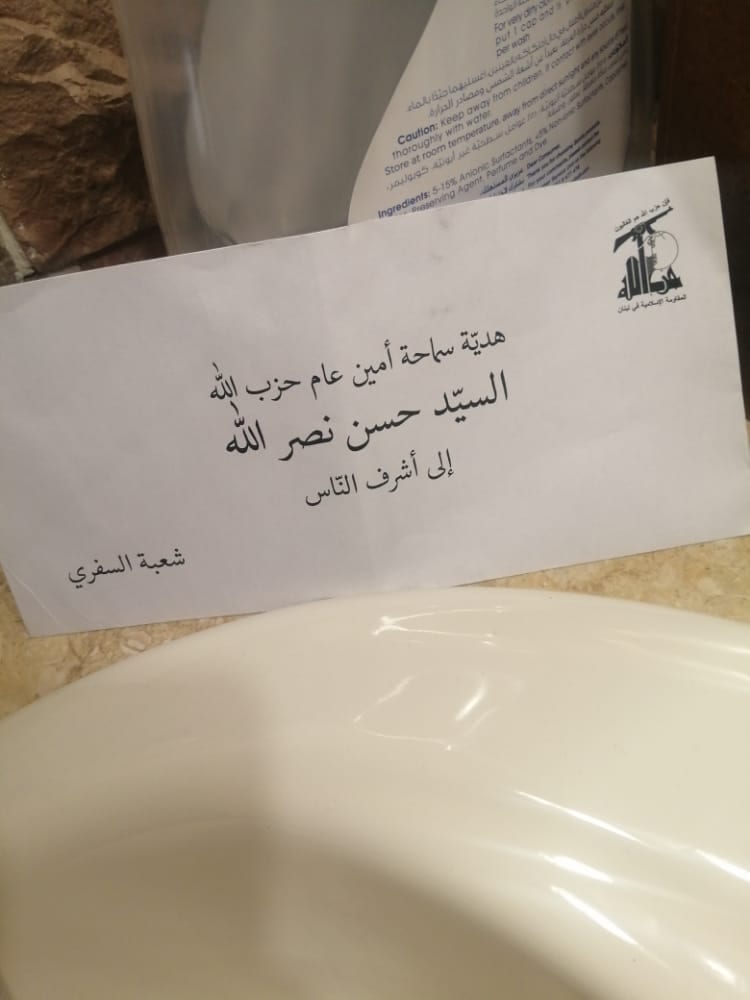

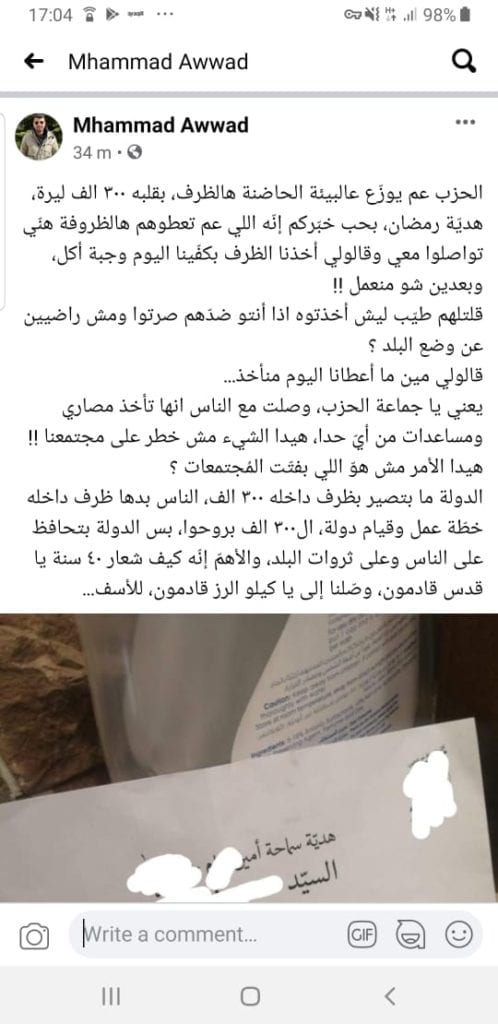

The party furthermore distributed envelopes containing 300,000 Lebanese pounds, as a gift from Hassan Nasrallah to “Ashraf Nass,” (honorable people). Hezbollah also distributed food boxes and gallons of oil bearing pictures of Nasrallah to its supporters.

With the increase in poverty and the worsening economic crisis, many people may default on their AQAH loans forcing the organization to confiscate the “pledged” gold or jewelry, and Hezbollah may have to use its money to cover depositors.

“The problem of default, especially seeing the current economic situation, means confiscating gold, and this reflects negatively on the party image,” said Hage Ali. “Such cases have already happened and are very harmful. Also, the problem here is twofold, because the gold often belongs to the woman, who is the weakest link in religious societies. Therefore, confiscating gold means inevitably robbing her of the little she owns, which produces a double injustice.”

Daher, however, ruled out that this will constitute a crisis for the party. The real danger of a crisis in the party, he said, lies in the distinction between those members who receive their salary in dollars and those who receive it in LBP.

This article is published with the support of the Adwaa Project.

Read Also:

{kind=link}